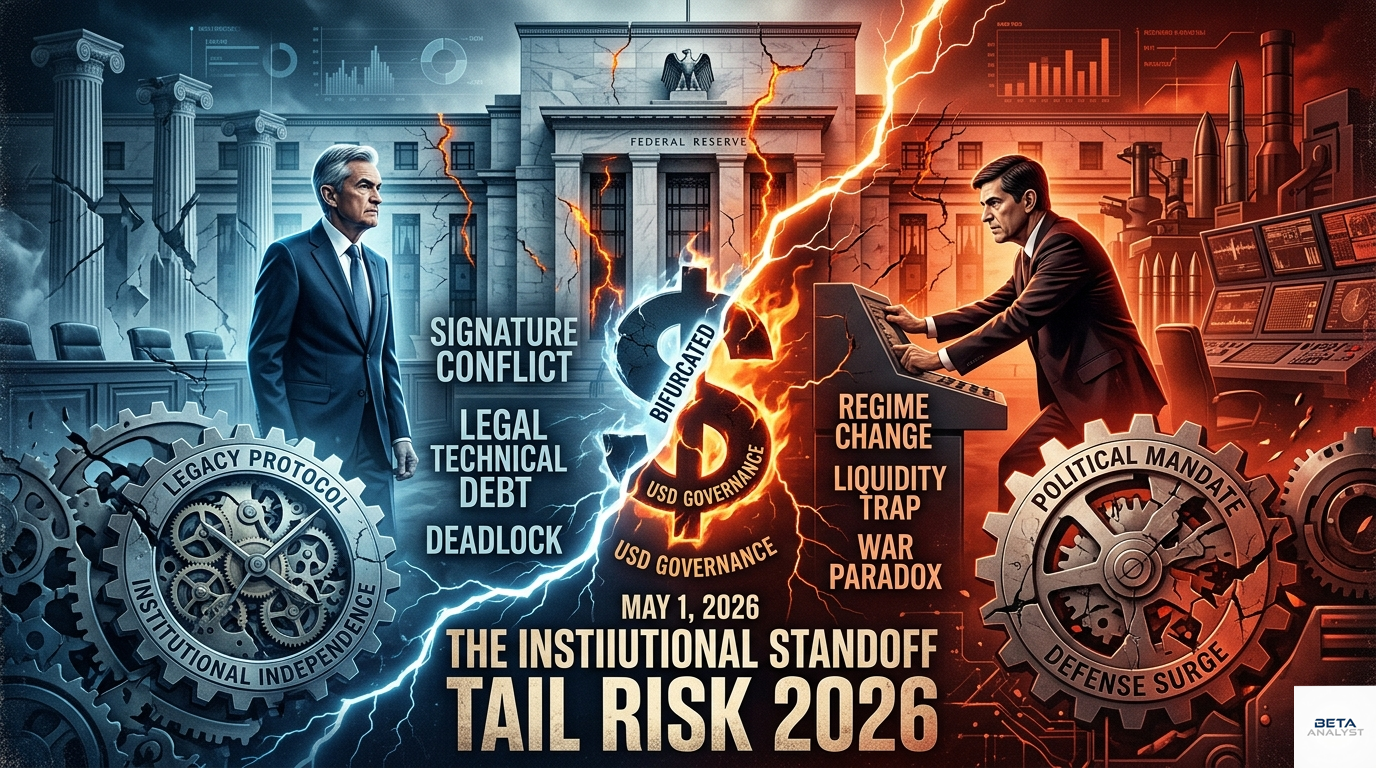

As of today, the Federal Reserve has ceased to function as a unified institution. It has entered a state of "institutional bifurcation"—a structural deadlock where two competing centers of authority are attempting to pilot the same ship.

While mainstream coverage remains fixated on the Department of Justice (DOJ) dropping its criminal probe into Jerome Powell last week (April 24), they are ignoring the more dangerous structural catastrophe occurring in the underlying "plumbing" of the US financial system. The May 15th transition is not a traditional handoff; it is a fundamental break in the chain of command for the US Dollar.

The Scene: Contested Authority at the Core

Following the Senate Banking Committee’s 13-11 party-line vote on April 29 to advance Kevin Warsh, the path to a new Chair is nominally clear. However, Jerome Powell’s unprecedented announcement that he will remain on the Board of Governors until 2028 creates a Signature Conflict that the global markets have yet to price.

Historically, outgoing Chairs resign from the Board to allow for a clean transition. Powell’s refusal—citing "institutional preservation" against "political encroachment"—means that for the first time in modern history, we will have a "Shadow Chair" with deep institutional loyalty sitting in direct opposition to a "Regime Change" Chair.

The Three Structural Flaws in the 2026 Financial Architecture

1. The Breakdown of Settlement Finality (The "Validity" Trap)

In high-stakes finance, "Finality of Settlement" is the bedrock of trust. When the Fed issues a directive, Primary Dealers (JPMorgan, Goldman Sachs, etc.) must trust that the signature behind that order is legally unassailable.

The April 29th FOMC meeting revealed four official dissents—the highest level of internal friction since 1992. This is a warning sign of a "governance fracture." If the FOMC is split down the middle, every "emergency" liquidity action led by Kevin Warsh could be challenged in court by the "Powell-aligned" minority. For a Treasurer at a Fortune 500 company, this introduces "Legal Technical Debt." If a bank acts on a directive that is later retroactively voided by a Supreme Court challenge, trillions in trades could become "zombie assets." This uncertainty is why we are seeing credit spreads widen; the market is pricing in the risk of a contested signature.

2. The Defense Priority Conflict (Liquidity Crowding)

The GOP’s FY2026 budget has authorized a staggering $1.5 trillion surge in Defense Industrial Base (DIB) spending. The strategy is clear: use the Defense Production Act to reorder market outcomes. While the incoming leadership is expected to aggressively cut rates to fund this munitions expansion, Powell’s presence on the Board acts as a Structural Firewall.

We are witnessing a "War Paradox." The government is trying to pivot to a war footing, which requires the Fed to monetize massive debt. However, with a contested leadership, the Fed cannot provide the clear, unified signal needed to calm the private markets. The result is a Liquidity Trap: Capital is being sucked out of private innovation and into government-mandated defense contracts, leaving the commercial sector to starve in a high-rate environment.

3. Institutional Gridlock and "Read-Only" Markets

The April FOMC statement was a masterclass in ambiguity. With one member voting for a cut and three others demanding even stricter anti-inflation measures, the Fed’s "consensus engine" has stalled.

When the leadership lacks a unified mandate, the entire financial system enters a "frozen" state. Decisions on credit facilities are delayed, policy language becomes dangerously vague, and the private market is left to speculate. In the volatile landscape of May 2026, speculation is the precursor to a systemic freeze.

The Strategic Conclusion: A Hard Fork in Governance

We are no longer debating interest rates; we are analyzing a Systems Failure. The standoff at 20th Street represents a "Hard Fork" in the governance of the US Dollar. On one side is the "Political Mandate" (Warsh/Defense Surge); on the other is the "Legacy Protocol" (Powell/Institutional Independence).

For CEOs, Treasurers, and International Investors, the primary risk is no longer "Will rates move?" The primary risk is: "Who actually owns the authority to honor the signature on my liquidity line?"

In a period of contested authority, the most valuable asset is not cash—it is clarity. And right now, the pipes are blocked.